OpenSea Shares Found on Offer at Steep Discounts as Brokers Skirt Restrictions

The meteoric rise of NFT marketplace OpenSea has been nothing short of astounding. Last valued at $13.3 billion after raising $300 million in early 2022, the company’s success has inspired awe and envy alike. But while its shares are closely held, they are not immune from the kinds of secondary market pressures that plague other hot startups.

SPVs Offer a Way Around Trading Restrictions

As reported by The Block in March, OpenSea shares and those of other leading crypto companies are being traded on brokerage platforms through Special Purpose Vehicles (SPVs). These bespoke legal entities are set up to facilitate secondary market transactions, allowing investors to buy and sell indirect interests in a private company’s stock.

The workaround is a source of tension between startups and their shareholders, with many well-capitalized companies forced to weather the market downturn without raising more money. Avoiding the dreaded “down round” is crucial because it involves raising money at a lower valuation than in previous rounds, which can be demoralizing for staff whose share options suddenly lose value.

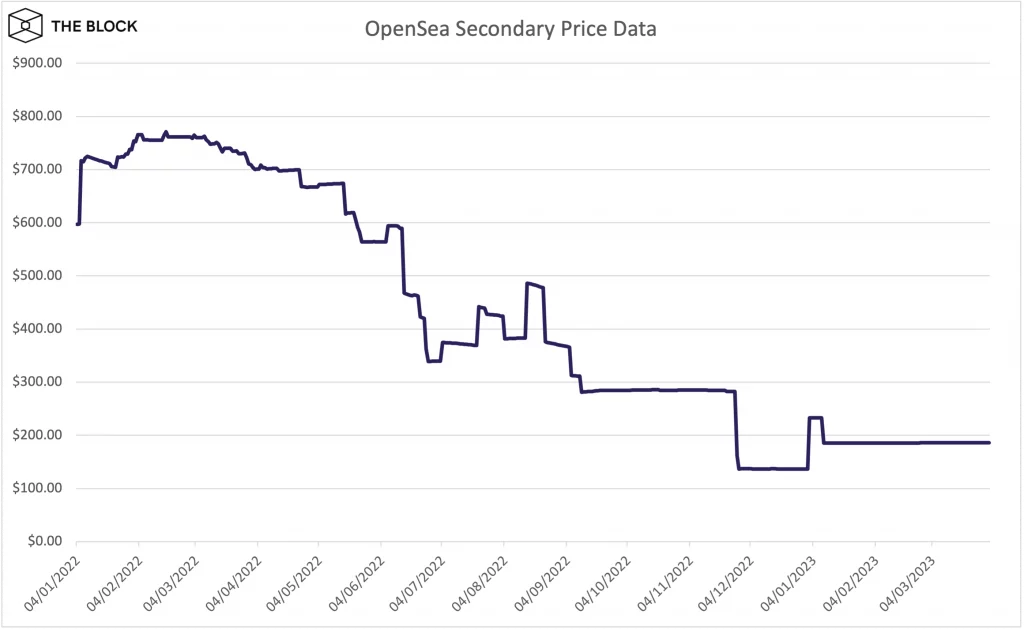

A Barometer for the Value of Startup Equity

But secondary market platforms such as Forge Global offer another barometer for the value of startup equity. Through these platforms, investors and employees can mark-to-market their shares. OpenSea is a prime example. The NFT company has managed to avoid raising money in the bear market, yet as of March 5, OpenSea shares were trading at a 51% discount on Birel, a secondary market platform for startup shares.

Dodging the Block

OpenSea has forbidden unsanctioned secondary sales since March 2021, but the bylaws of the corporate entity behind OpenSea, Ozone Networks, Inc., state that a stockholder shall not transfer any shares of the corporation’s stock or any rights of or interest in such shares to any person unless such transfer is approved by the board of directors.

According to Birel CEO Richard Freemanson, many companies do not want deals in the secondary market, so they prohibit it. However, some OpenSea shareholders interested in an exit offer allocations via SPV, and rarely through forward contracts, to ensure that the deal is not blocked by the company.

Investors Want Direct Access to Shares

Some investors are less than thrilled with the SPV setup, which they claim fragments liquidity and hinders trading. According to one anonymous source, 95% of OpenSea shares trading on secondary markets take the form of SPVs, with each lot attached to its own entity. This results in additional fees and less control. Another investor, a founder and angel investor in fintech firms, said investors would prefer to buy shares directly as they are one step removed from the actual investment, which just isn’t ideal.

Conclusion

In short, while OpenSea and other well-capitalized startups may appear invincible, they are not immune from the vagaries of the secondary market. Brokers are using SPVs to offer investors a way around trading restrictions, but the setup is not without its detractors. Investors want direct access to shares, and SPVs come with additional fees and less control. It remains to be seen how companies like OpenSea will address these challenges, but one thing is certain: the market never stands still.

Source: The Block

{kind=link}